Advertisement

CBK explains why most Kenyans are limited to cash advance

29th September, 2025 01:20 PM

The Central Bank of Kenya (CBK) has shared a detailed explanation on why a number of Kenyans are limited to advance offerings, linking it to mobile money transactions.

In a document released to the public on Monday, September 29, 2025, by the Kenya National Financial Inclusion Strategy 2025-2028, the regulator has stated that most Kenyans still use mobile money primarily for basic services like person-to-person transfer, with limited advanced offerings.

Also Watch: CBK invites public input on draft national financial inclusion strategy 2025–2028

“Recent data shows signs of plateauing growth in mobile money access and usage. Most users still rely primarily on basic services like person-to-person transfers, with limited uptake of advanced offerings such as digital credit, insurance, or savings,” CBK noted.

While further adding that the limitations has attributed to issues such as limited interoperability, high transaction costs, low financial literacy, and product designs that do not reflect the realities of underserved groups.

“This is attributed to issues such as limited interoperability, high transaction costs, low financial literacy, and product designs that do not reflect the realities of underserved groups,” CBK said.

Worth noting, currently, charges on some mobile money transfers can reach as high as 6.9 per cent of the transaction amount, considerably higher than the fees banks charge for retail cash movements.

Also Watch: CBK raises lending rate from 8.75% to 9.5%

The Central Bank of Kenya has revealed that this pricing structure has contributed to the plateauing growth of mobile money usage.

“Most users still rely primarily on basic services like person-to-person transfers, with limited uptake of advanced offerings such as digital credit, insurance, or savings,” CBK said.

On the other hand, CBK noted that this stagnation is attributed to factors including high transaction fees, limited interoperability, and financial products that do not fully meet the needs of underserved populations.

M-Pesa dominates the market with more than 90 percent of mobile money transactions, underscoring Safaricom’s dominant position.

The CBK has highlighted that Mobile money is the single most transformative tool for financial inclusion having expanded access to financial services for millions of Kenyans since its inception in 2007.

“Mobile money is the single most transformative tool for financial inclusion,” CBK stated.

CBK fees waived during COVID-19

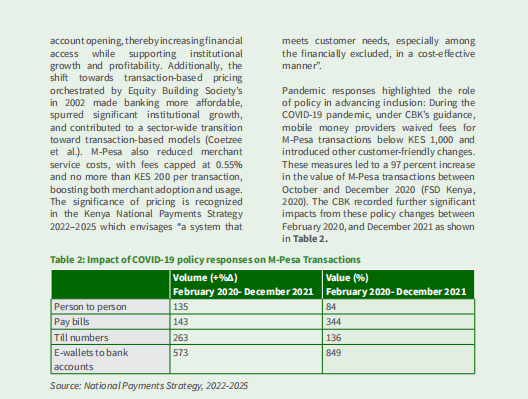

The controller further revealed that during the early phase of the COVID-19 pandemic, the CBK waived fees on transactions up to 1,000 shillings between March 2020 and December 2022, which helped increase active users by over 6.2 million.

However, the monthly volume of person-to-person transactions also soared from 162 million to 440 million, with values increasing from 234 billion to 399 billion shillings.

CBK noted that despite the reintroduction of fees in 2023, they remain significantly lower than pre-pandemic levels.

Meanwhile, according to the Communications Authority of Kenya, mobile money subscriptions currently stand at 47.7 million, representing a penetration rate of 91 per cent.