Advertisement

CBK’s new pricing model ends lower loan rates for bank staff

03rd September, 2025 10:51 AM

Caption:CBK scraps bank staff loan benefits in new model. VIDEO/K24TV The Central Bank of Kenya (CBK) has scrapped preferential loan terms for bank employees under its revised Risk-Based Credit Pricing Model (RBCPM), which came into effect on September 1, 2025.

In an official statement released on August 26, 2025, CBK announced that the updated RBCPM aims to strengthen the transmission of monetary policy, enhance transparency in lending practices, and encourage responsible borrowing by tying credit pricing to the risk profiles of borrowers.

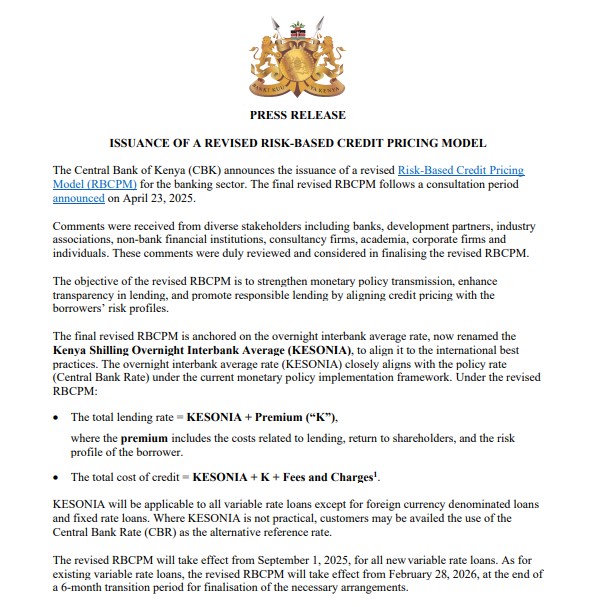

“The Central Bank of Kenya (CBK) announces the issuance of a revised Risk-Based Credit Pricing Model (RBCPM) for the banking sector. The final revised RBCPM follows a consultation period announced on April 23, 2025,” the CBK statement reads.

“The objective of the revised RBCPM is to strengthen monetary policy transmission, enhance transparency in lending, and promote responsible lending by aligning credit pricing with the borrowers’ risk profiles.”

In addition, CBK said the final revised pricing model is anchored on the overnight interbank average rate, now renamed the Kenya Shilling Overnight Interbank Average (KESONIA), to align with international best practices.

It added that KESONIA closely aligns with the Central Bank Rate under the current monetary policy framework.

“The final revised RBCPM is anchored on the overnight interbank average rate, now renamed the Kenya Shilling Overnight Interbank Average (KESONIA), to align it to the international best practices,” the CBK’s statement reads.

“The overnight interbank average rate (KESONIA) closely aligns with the policy rate (Central Bank Rate) under the current monetary policy implementation framework.”

Lending framework

The Central Bank further explained that under the revised model, the total lending rate will be calculated as KESONIA plus a premium covering lending costs, shareholder returns, and the borrower’s risk profile, while the total cost of credit will be KESONIA plus the premium, fees, and charges.

“Under the revised RBCPM, the total lending rate = KESONIA + Premium (“K”), where the premium includes the costs related to lending, return to shareholders, and the risk profile of the borrower. The total cost of credit = KESONIA + K + Fees and Charges, “CBK explained.

According to the Central Bank stated that KESONIA will apply to all variable-rate loans except foreign-currency-denominated and fixed-rate loans, adding that where its use is not practical, customers may instead use the Central Bank Rate as the alternative reference rate.

“KESONIA will be applicable to all variable rate loans except for foreign currency denominated loans and fixed rate loans. Where KESONIA is not practical, customers may be availed the use of the Central Bank Rate (CBR) as the alternative reference rate,” CBK stated.

Implimentation

In addition, CBK stated that the revised lending model took effect on Monday, September 1, 2025, for all new variable rate loans, while existing variable rate loans will transition to the new model on February 28, 2026, after a six-month adjustment period.

“The revised RBCPM will take effect from September 1, 2025, for all new variable rate loans. As for existing variable rate loans, the revised RBCPM will take effect from February 28, 2026, at the end of a 6-month transition period for finalisation of the necessary arrangements,” CBK added.

“To ensure transparency, the banks will publish on their websites and on the Total Cost of Credit (TCC) website, their weighted average lending rates, weighted average premium (K), and fees and charges for each of their lending products.”