Advertisement

Explained: Difference between a credit card and a debit card

30th April, 2026 02:34 PM

At first glance, a credit card and a debit card look almost identical. Both can be used to pay for shopping, fuel, online subscriptions or even food delivery.

But the real difference is simple and powerful: where the money comes from.

Understanding this difference can help you avoid debt, manage your spending and make smarter financial decisions.

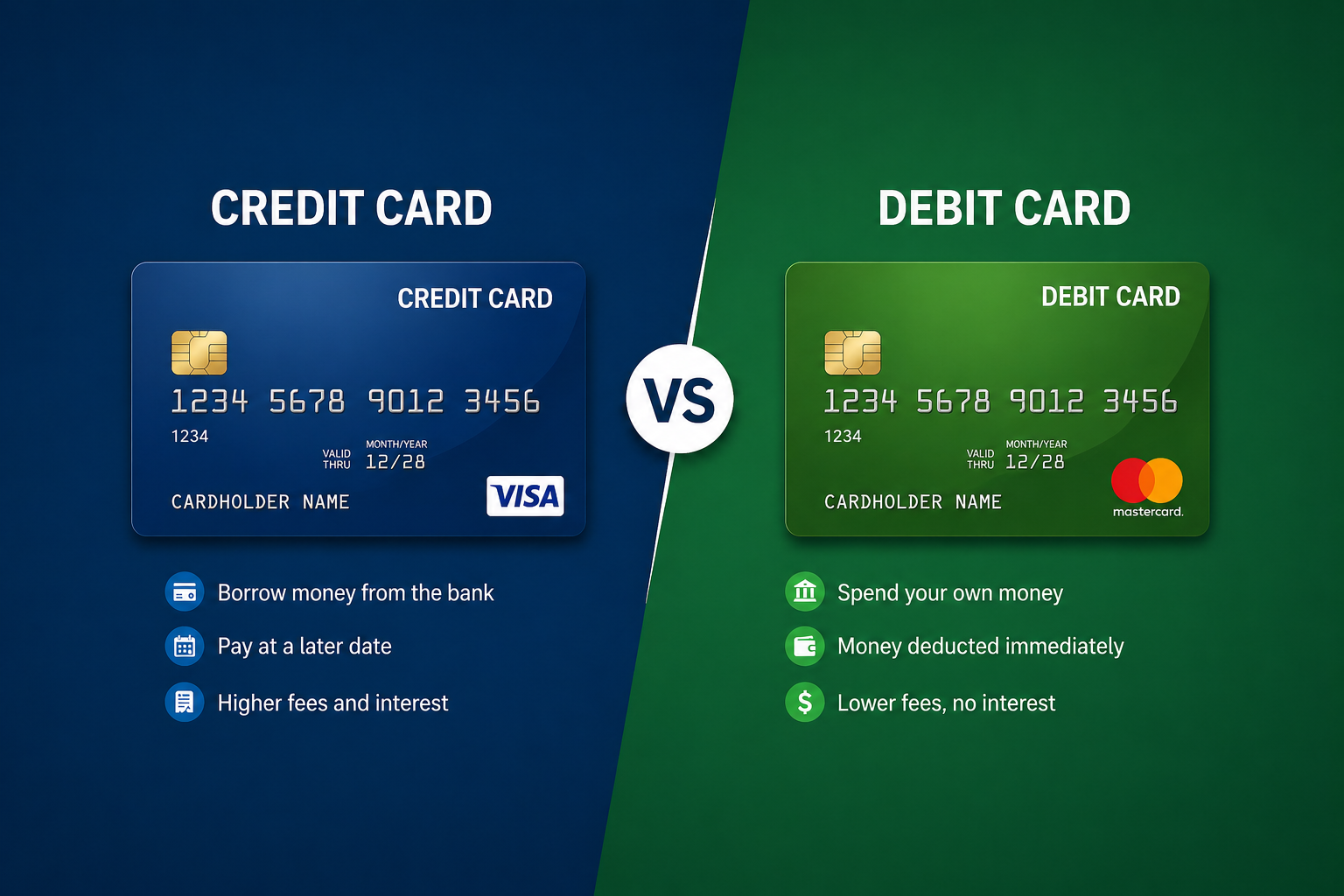

Where the money comes from

This is the biggest difference.

A debit card uses your own money. When you pay for something, the money is taken directly from your bank account instantly.

A credit card uses borrowed money from the bank. You spend now, then repay later, either in full or over time.

Think of it this way:

If you have Ksh2,000 in your account and swipe a debit card for Ksh1,500, your balance drops to Ksh500 immediately.

But if you use a credit card for the same Ksh1,500, the bank pays first, and you owe them that money later.

Simple real-life example

Imagine you want to buy shoes worth KSh5,000.

With a debit card:

You must already have KSh5,000 in your account. If you do not, the transaction may fail.

With a credit card:

You can still buy the shoes even if your account has less money, as long as your credit limit allows it. You will pay the bank later.

Spending control vs borrowing freedom

Debit cards naturally help with budgeting because you can only spend what you have.

This reduces the risk of falling into debt.

Credit cards offer flexibility. You can handle emergencies or big purchases even when you are short on cash.

However, if not managed well, they can lead to debt because you are borrowing money.

Interest and fees

Debit cards usually have no interest charges because you are not borrowing money.

Credit cards, however, may charge interest if you do not repay the full amount on time. They can also come with fees such as late payment charges.

This is why many financial experts advise paying your credit card bill in full each month.

Impact on your financial future

Using a debit card does not build your credit history because you are spending your own money.

A credit card can help build your credit score if used responsibly.

Paying on time shows lenders you can manage borrowed money. Missing payments, however, can damage your financial reputation.

Safety and protection

Both cards are generally safe, but credit cards often offer stronger fraud protection and extra benefits like rewards or cashback.

With a debit card, fraud can directly affect your bank balance, so quick reporting is important.

Final understanding

A debit card is about control. You spend what you have.

A credit card is about trust. You spend what you promise to repay.

Neither is better in all situations. The best choice depends on how well you manage money.

If used wisely, both can work together to make your financial life easier and more secure.