Advertisement

How to financially prepare your family for your death in Kenya

18th July, 2026 12:51 PM

Losing a loved one is hard enough without the added weight of an immediate financial crisis. In Kenya, many families find themselves locked out of bank accounts, mobile money wallets, and family land simply because a relative died without leaving clear records.

While discussing death is uncomfortable, putting a solid financial plan in place keeps family wealth safe. In fact, peer-reviewed research shows that early preparation “promotes an efficient estate administration process that benefits the next of kin, enabling the inherited wealth to be utilised.”

Taking control of documentation ensures dependents do not suffer. The Law of Succession Act came into force on July 1, 1981, to guide inheritance, yet family splits over frozen cash remain a daily reality.

Securing local assets and document access

The most important step is updating nominee details on every financial account. Whether it is an active bank account, a Sacco membership, or a mobile money profile, financial institutions need a designated name to hand over funds.

Without a registered nominee, a balance as small as Ksh50000 can stay frozen for months during court processes.

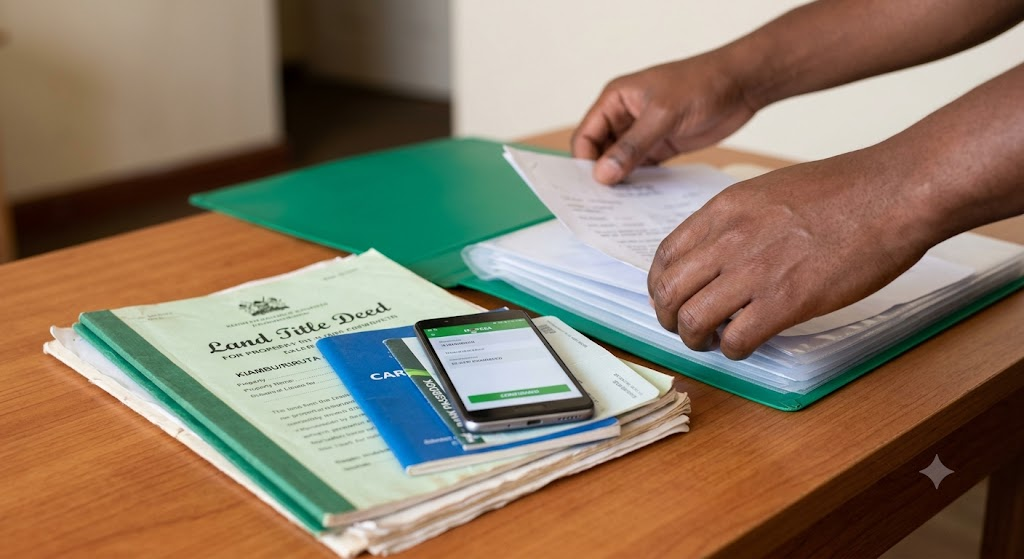

Families also need a single list showing where to find vital papers. Relatives must know exactly where to locate title deeds, logbooks, share certificates, and national identity cards.

Leaving a hidden investment does no good if nobody knows it exists. Sharing digital account access information prevents modern assets from disappearing too. Relatives often lose business pages, digital savings, and phone wallets because passwords were kept secret.

A simple master file shared with a trusted person keeps these assets safe.

Navigating international planning for the diaspora

Kenyans living abroad face unique legal hoops when securing their wealth. A diaspora citizen might own properties in Nairobi while holding bank accounts in London or New York. This splits their estate across different legal systems.

When a diaspora citizen passes away, the local family often lacks the legal knowledge required to claim foreign funds, sometimes running into administrative fees reaching upwards of USD2000.

Global assets must align with Kenyan laws to avoid long court battles. Holding funds in joint accounts with a survivorship clause or setting up international trusts helps transfer money smoothly without needing foreign court interventions.

Every diaspora investor should ensure their global assets are easy to trace, with clear steps for local relatives. Taking these actions guarantees that hard-earned money remains a blessing rather than a legal headache.