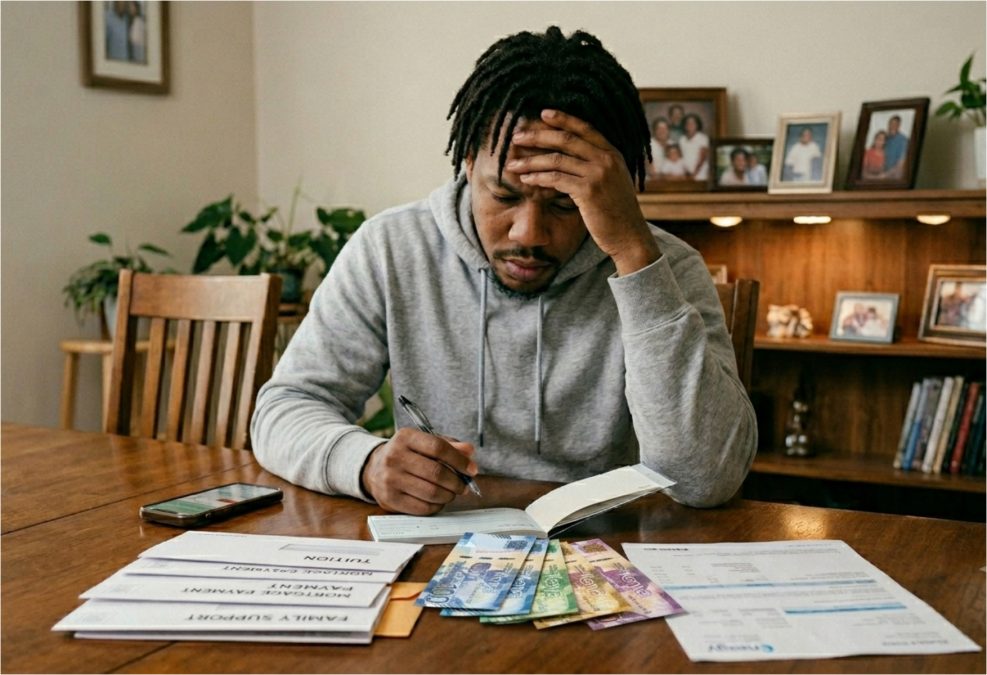

Financial mistakes Kenyans make in their 20s and how to fix them

By Katemarthason Okudo, July 13, 2026The 20s are often seen as the decade of first salaries, greater independence and exciting new experiences. It is also the period when many people begin making financial decisions without much guidance. While earning an income is an important milestone, the habits formed during these early working years can influence financial stability for decades.

Many young Kenyans focus on meeting immediate needs or enjoying the rewards of employment, but experts say this is also the best time to build healthy money habits. According to the Kenya National Bureau of Statistics (KNBS), digital lending and changing spending patterns have significantly influenced how young adults manage their finances, making financial literacy more important than ever.

Depending on mobile loans too early

One of the most common mistakes is turning to mobile loans before building an emergency fund. Easy access to digital credit can make borrowing feel like a quick solution for everyday expenses, but repeated borrowing often creates a cycle that becomes difficult to escape.

Financial experts recommend setting aside money for unexpected costs before relying on credit. Even saving a small amount every month can help cover emergencies such as medical bills, transport or urgent household expenses without borrowing.

Responsible borrowing should only happen when there is a clear repayment plan, while savings should remain the first line of defence against unexpected financial shocks.

Spending every salary increase

Receiving a salary increment is a rewarding moment, but many people immediately increase their spending. A bigger house, expensive gadgets or frequent dining out can quickly consume the extra income.

Instead, financial planners encourage increasing savings whenever income rises. Allocating part of every salary increment to investments, savings accounts or retirement plans allows wealth to grow steadily over time.

The OECD notes that consistent investing, even in small amounts, can build long-term financial security through the power of compounding.

Waiting too long to save for retirement

Retirement often feels too far away for someone in their 20s. As a result, many postpone pension contributions until later in life.

However, delaying retirement savings by several years means missing valuable time for investments to grow. Starting early, even with modest contributions, gives savings more time to earn returns.

According to Kenya’s Retirement Benefits Authority (RBA), beginning pension contributions early can significantly improve financial security after retirement because of compound growth over many years.

Trying to keep up with social spending

Weekend outings, buying rounds of drinks, attending every event or constantly spending to match friends can quietly drain a young person’s income. While social activities are important, regularly spending beyond one’s budget leaves little room for saving.

Creating a monthly entertainment budget allows people to enjoy social life without sacrificing financial goals. Learning to say no to unnecessary expenses can make a significant difference over time.

The Kenya Bankers Association (KBA) encourages budgeting and tracking expenses as practical ways of avoiding lifestyle inflation and improving financial discipline.

Ignoring a personal budget

Many young adults know how much they earn but have little idea where the money goes. Without a budget, small daily expenses gradually consume income before savings are made.

A simple monthly budget that prioritises essential bills, savings and investments before discretionary spending provides greater control over finances. Reviewing spending regularly also helps identify unnecessary expenses that can be reduced.

Budgeting is one of the most effective ways to strengthen financial wellbeing and reduce money-related stress.

Building better financial habits

Financial mistakes made in the 20s do not have to define the future. Breaking the habit of unnecessary borrowing, saving before spending, investing early and living within one’s means can gradually improve financial stability.

The earlier these changes begin, the more time money has to grow. Small, consistent financial decisions made today can create greater opportunities, reduce future financial pressure and provide lasting peace of mind.