How to raise children who understand the value of money

By Dan Kauna, May 1, 2026There is a familiar scene in many Kenyan homes. A child tugs at their parent’s sleeve at the supermarket checkout, pointing at a snack or a toy.

The parent either gives in or says no without explanation, and the moment passes.

What rarely happens is the conversation in between. The one that could teach the child something lasting about money.

Research shows that children’s financial habits begin forming as early as age seven.

“By the age of seven years, several basic concepts relating broadly to later ‘finance’ behaviours will typically have developed.” Whitebread & Bingham say in Habit Formation and Learning in Young Children, University of Cambridge/Money Advice Service, 2013.

That means the window is already open in most Kenyan homes, and the parents who use it have a real head start.

Financial literacy is not a subject reserved for economics class or adulthood. Children who grow up understanding money (where it comes from, how it is managed, and why it runs out) tend to make smarter decisions as adults.

The good news is that you can start at home with your child, using everyday Kenyan life as your classroom.

Start with the simple things

You do not need a formal curriculum to begin. The mkokoteni vendor, the matatu fare, the mama mboga stall down the road – these are all live lessons waiting to happen.

Start by letting your child handle small amounts of money.

Give a seven-year-old Ksh 50 and ask them to buy a specific item from the shop. Walk them through calculating, asking for and receiving change.

Let them feel the weight of a financial transaction, even a small one.

From there, you can introduce the idea of budgeting.

A simple approach is the three-jar method – one jar for spending, one for saving, and one for giving.

It sounds basic, but it builds a habit of thinking about money in categories rather than as one undifferentiated resource to be spent immediately.

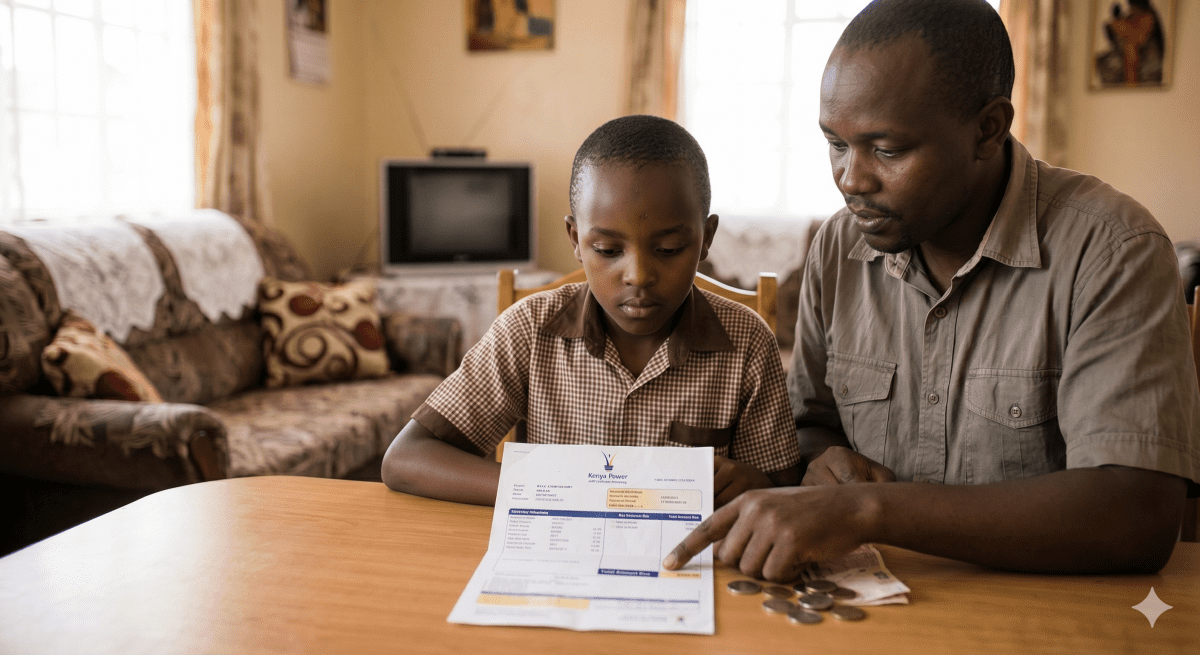

Older children, from around ten years upward, can handle more nuance. Talk to them about household bills. You do not have to share exact figures if you are not comfortable, but showing them that electricity, water, and food cost money every month normalises the reality that income is finite. A child who sees their parent pay the KPLC bill understands, in a real way, that lights are not free.

Make it feel real, not like a lecture

The biggest mistake parents make is turning money lessons into a sermon.

Children switch off quickly when they feel they are being lectured. The goal is to weave financial thinking into daily life so naturally that it does not feel like a lesson at all.

Take your child shopping and give them a small budget to manage. Ask them to compare prices on the shelf.

Let them make a choice and live with it, even if they later wish they had chosen differently. That small frustration is far more instructive than any amount of advice.

You can also use relatable goals. If your child wants a toy or a game that costs Ksh 500, help them work out how many weeks of pocket money it would take to save for it.

Suddenly, patience and planning have a purpose they care about.

The stakes are real.

Access to money and knowing what to do with it are two very different things, and that gap begins in childhood.

The parent who starts these conversations early is doing something that no school curriculum or mobile app can fully replace.