Advertisement

When money decisions feel heavy: Understanding financial paralysis

26th May, 2026 12:11 PM

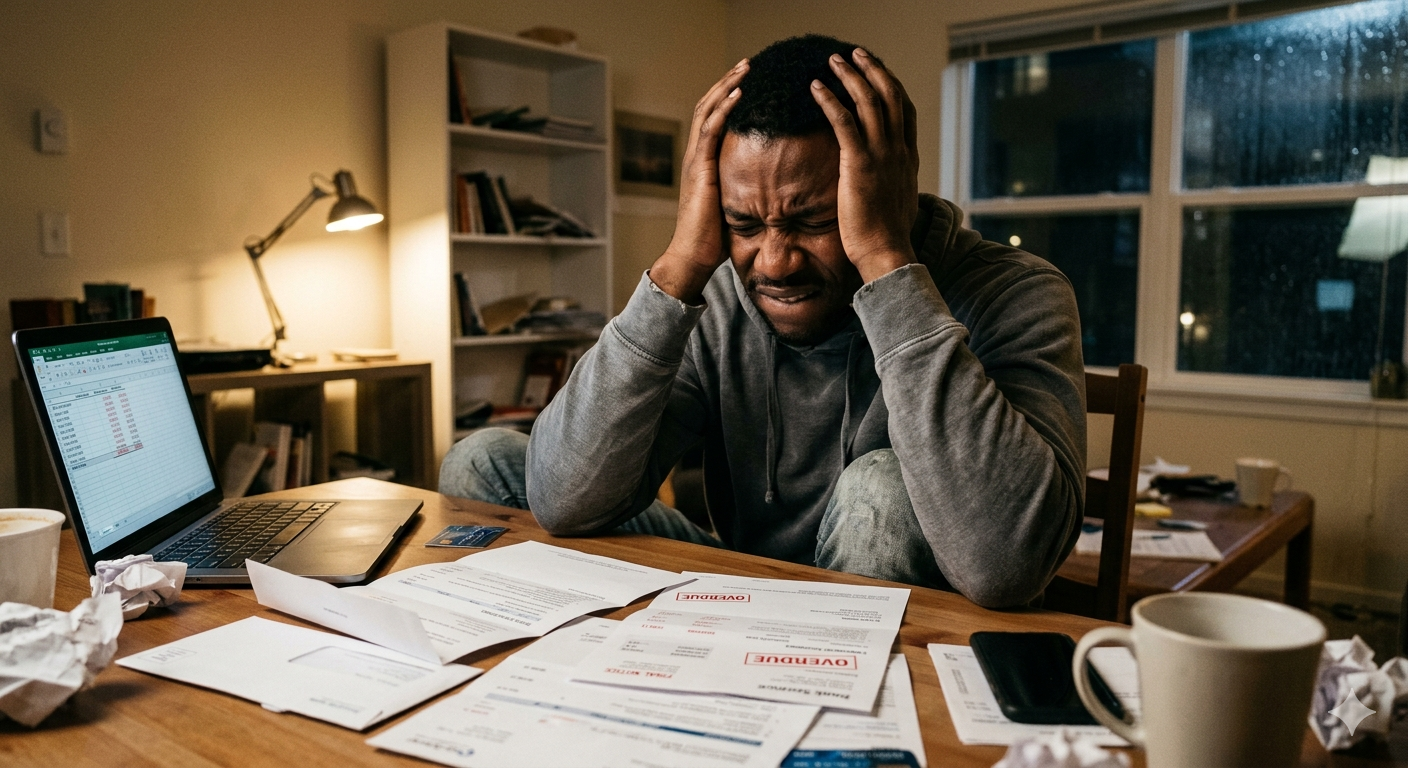

There is a growing but often unspoken struggle affecting many people today: money paralysis. It is the feeling of being mentally stuck when it comes to making financial decisions, even simple ones like saving, spending, or investing.

In a time where expenses keep rising, and income rarely feels enough, many people find themselves delaying or avoiding financial choices altogether.

Financial wellness experts describe money paralysis as a mental freeze caused by fear, uncertainty, or lack of financial knowledge.

“Money paralysis is when individuals feel overwhelmed to the point where they avoid making financial decisions, even when action is necessary,” Financial Literacy Reports stated.

This condition does not only affect low-income earners. It cuts across different income levels, especially where budgeting is unclear or financial pressure is constant.

The pressure of rising costs and limited income

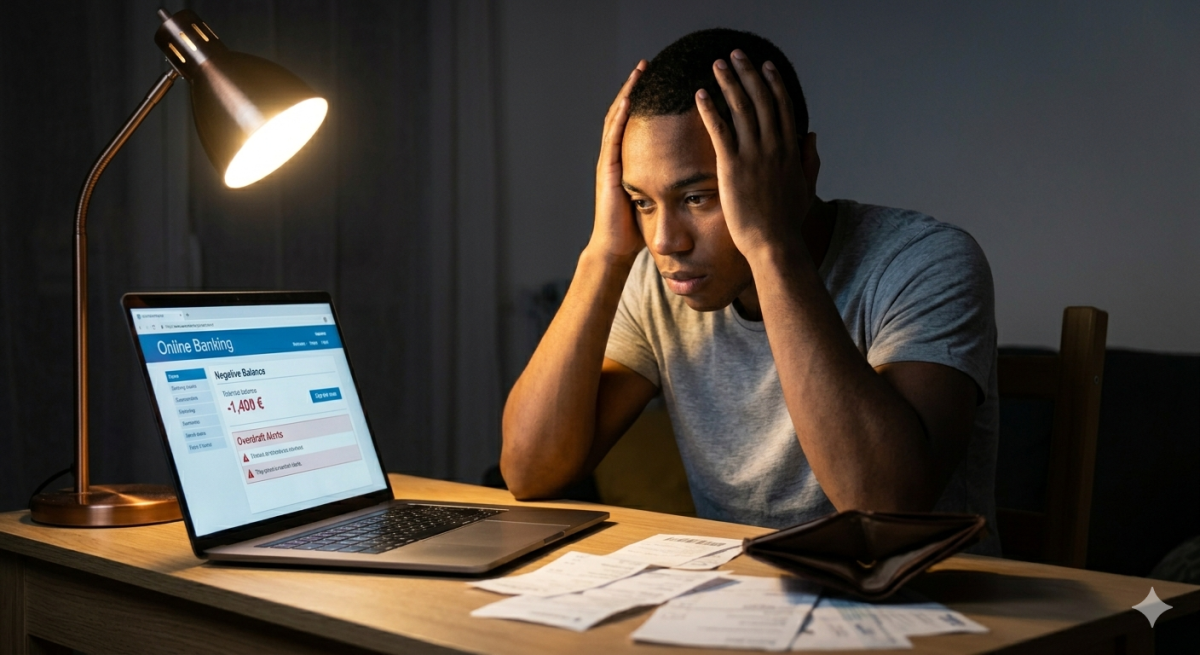

One of the biggest triggers of money paralysis is the rising cost of living. Rent, transport, food, and utility bills continue to increase, while incomes remain static for many households.

This creates a cycle where people feel there is never a “right time” to make financial plans.

Reports on financial inclusion by World Bank show that many individuals globally struggle with financial confidence, leading to poor or delayed financial decisions.

In Kenya and other developing economies, informal financial pressures add even more strain, making planning feel like guesswork rather than control.

When every shilling has multiple demands attached to it, even simple decisions like saving a small amount or starting an investment plan can feel overwhelming.

Avoidance as a coping mechanism

Instead of facing financial decisions head-on, many people tend to avoid them. This avoidance may look like ignoring bank notifications, postponing budgeting, or delaying investment opportunities.

While it may provide temporary emotional relief, it often worsens financial stress in the long run.

Avoidance becomes a coping mechanism when financial stress feels too heavy to process.

This cycle continues quietly, where fear leads to delay, and delay leads to more pressure.

Eventually, individuals feel even less in control of their money, deepening the paralysis.

Breaking the cycle through small steps

Experts suggest that overcoming money paralysis does not require sudden big changes.

Instead, small consistent actions can help rebuild financial confidence. This includes tracking daily spending, setting realistic savings goals, or seeking basic financial education.

Financial institutions continue to promote financial literacy programs aimed at helping individuals make informed money decisions and reduce anxiety around finances.

Breaking the cycle begins with acknowledging the problem and taking small, manageable steps instead of waiting for the “perfect financial moment,” which rarely comes.