How to financially prepare for job loss before it happens

By Dan Kauna, May 15, 2026Losing a job is rarely something you see coming.

One month you are counting on that salary; the next, you are doing the maths on how long your savings will carry you.

In Kenya’s current job market, employment disruption is not a remote concern. For many workers, it is one restructuring or one non-renewed contract away.

The smartest financial preparation happens well before the crisis arrives, not during it. Here is where to start.

Build an emergency fund that can actually carry you

The standard advice (“save three to six months of living expenses”) exists because the research consistently backs it.

A 2025 study by Vanguard Research, drawing on a survey of more than 12,000 investors, found that “emergency savings are the strongest predictor of financial well-being,” outperforming income level, financial assets, and even debt profile.

The same study found that workers without a savings cushion spend four times as many hours distracted by financial stress at work, which creates its own professional risk on top of the financial one.

What does this look like in practice? Work backwards from your monthly fixed costs: rent, transport, food, utilities, and any loan repayments. If those total Ksh45,000, your emergency fund target sits between Ksh135,000 and Ksh270,000.

That figure sounds large, but it is not meant to be saved in one go.

A standing order, even Ksh3,000 to 5,000 a month into a money market fund, builds it steadily without requiring discipline every time.

Test your freelance income and review your insurance cover

A side income that only exists on paper offers almost no financial protection. The real buffer is one that has already earned real money.

A GeoPoll survey conducted across all 47 Kenyan counties in November 2024 found that 71 per cent of adults aged 18 to 35 have a side hustle, but earning capacity and consistency vary sharply.

Before a job loss forces the question, put yours to a real test: can it generate income this month without your main job propping up your time, energy, or confidence? If the answer is not clear, now is the time to find out.

Skills diversification sharpens this further.

Short professional certifications (in project management, data analysis, digital marketing, or a hands-on trade) expand the number of doors available to you in an active job search. They also reduce the gap between positions.

A 2024 study published in JAMA Network Open by researchers at Johns Hopkins Bloomberg School of Public Health found that people who had experienced income or job loss carried psychological distress scores that were “1.09 and 1.11 times higher” years after the event compared to those who had not, which makes the case not just for financial preparation, but for active career hedging as a form of mental health protection.

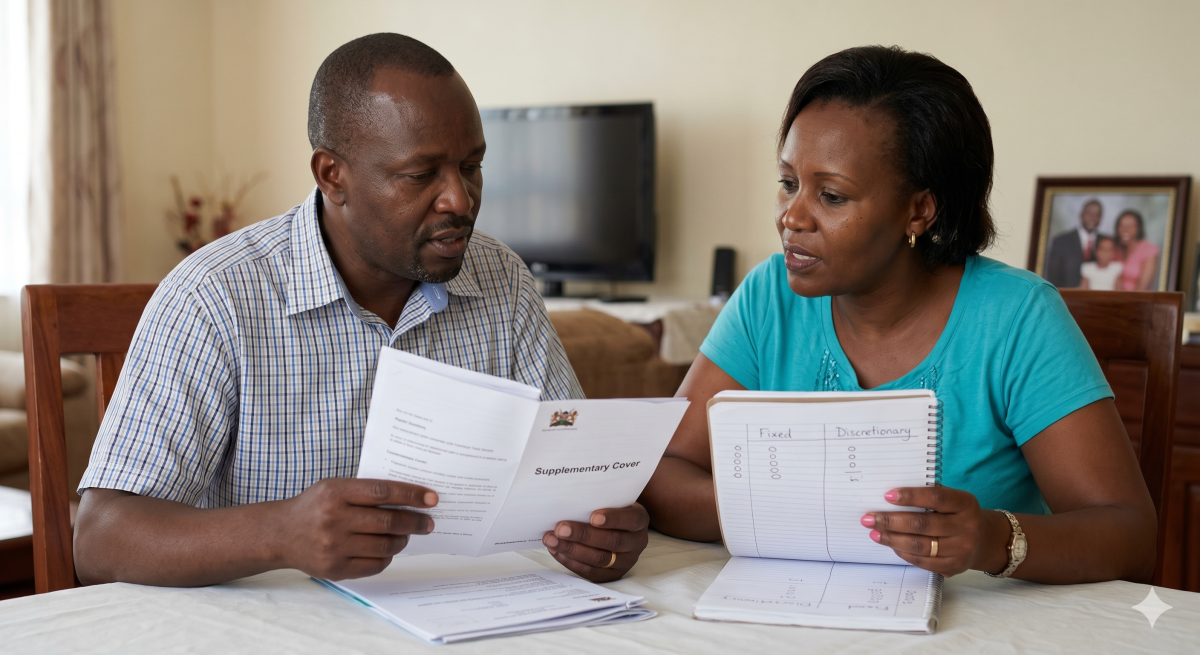

Finally, review your insurance. Your employer’s group medical cover ends the day your job does.

Sit with your budget now and separate what is truly fixed from what is discretionary. Knowing exactly which expenses can be trimmed in an emergency (and which cannot) means you will not be making those decisions under pressure.